by James Elliot (Head of Multi-Asset) and Iain Cunningham (Portfolio Manager Multi-Asset) from Ninety One

THE FAST VIEW

- Economies have rebounded strongly since March 2020, and this should accelerate in the second half of 2021 as vaccination programmes gain traction.

- Pent-up demand for services and excess savings should provide further support for the recovery as social-distancing measures are eased.

- Major central banks are likely to remain highly accommodative, with tapering only expected in 2022; we expect real interest rates to remain very low versus history.

- Near-term inflation may well rise, but this is more due to the current price level being contrasted against sharp price declines during the COVID-19 shock.

- It is important to closely monitor the Chinese market; the Chinese credit cycle has strongly influenced the global cycle as its impact has grown over the past decade.

March 2020 marked the point of maximum pain for the global economy and financial markets as governments issued lockdown orders in seeking to contain COVID-19. Subsequently, governments and central banks eased policy quickly and aggressively through fiscal and monetary measures, respectively, in seeking to backstop economies and ensure functional financial markets. Economies around the world have rebounded strongly since, initially in a V-shape, followed by more bumpy progress as localised lockdowns have been put in place. The release of better-than-expected vaccine trial results in November, and the subsequent roll-out of vaccination programmes have enabled financial markets to look through recent economic volatility and begin to discount a likely acceleration of the economic recovery in the second half of this year.

RECOVERY WILL BE SUPPORTED BY PENT-UP DEMAND

Looking forward, vaccine programmes are set to reach the point where a return to normality in major developed markets (assumed as 70-85% vaccination rates among populations) can be achieved within the coming months. The US and UK are leading, with Europe – after its slow start – likely reaching this point by September. As this takes place there will likely be an acceleration in the recovery supported by pent-up demand particularly for services, with policy measures remaining highly accommodative.

The extent of the fiscal and monetary measures that authorities implemented as a response to the pandemic a year ago gave us confidence to take on risk in our strategies. The impact on the real economy has since been evident; never before has a sharp rise in US aggregate disposable income taken place at the same time as a significant rise in the unemployment rate. The US administration, under President Biden, has since doubled down on fiscal support with an additional relief package and, as a result, average US household disposable income is 7% higher than at the start of last year, while the unemployment rate is now 6.2% versus 3.6% over the same period. This dynamic is somewhat similar in other major nations where savings rates have spiked (Figure 1), and we estimate that the aggregate income that has yet to be spent (excess savings) to be c.7.5%, c.7.7% and c.4% of GDP in the US, UK and Eurozone, respectively. These savings should add impetus to pent-up demand and the recovery as social-distancing measures are removed through the rest of this year.

FED TAPERING IS UNLIKELY TO COME THIS YEAR

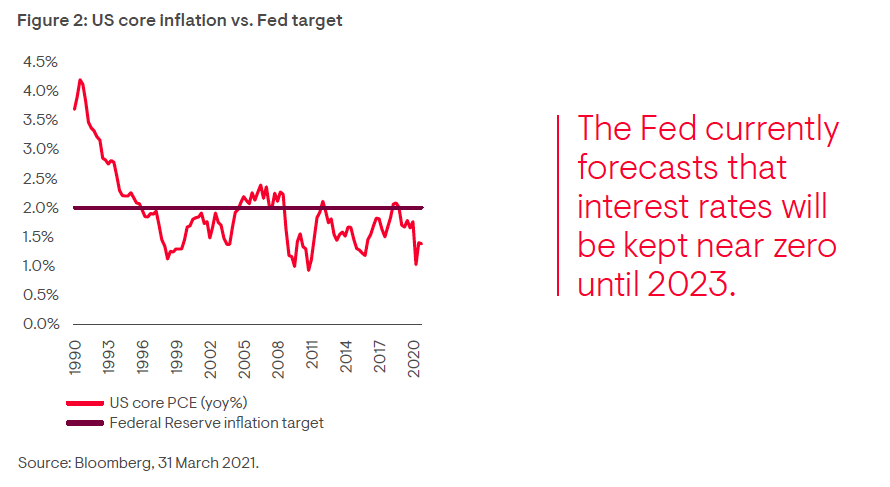

At the same time, central banks are generally committed to maintaining highly accommodative policy well into the recovery in the coming years. To date, major central banks have slashed interest rates and created US$9 trillion, which has aided the economy, ensured easy financial conditions, and ultimately inflated asset prices. Major central banks have committed to print money until the end of 2021, before likely tapering next year, and keeping interest rates at their current level for some time. We continue to believe that the Federal Reserve’s (Fed) policy framework review remains underappreciated by investors; it has committed to achieving an average core inflation rate of 2% over time, yet historically this has not been achieved (Figure 2). As a result, the Fed currently forecasts that interest rates will be kept near zero until 2023. We believe it will keep policy loose relative to economic fundamentals for at least the next 12-18 months in seeking to deliver an inflation overshoot, which will likely keep real interest rates very low versus history. Such an environment has historically been constructive for risk assets and has ultimately fostered speculative activity.

INFLATION SPIKES ARE LARGELY DOWN TO BASE EFFECTS

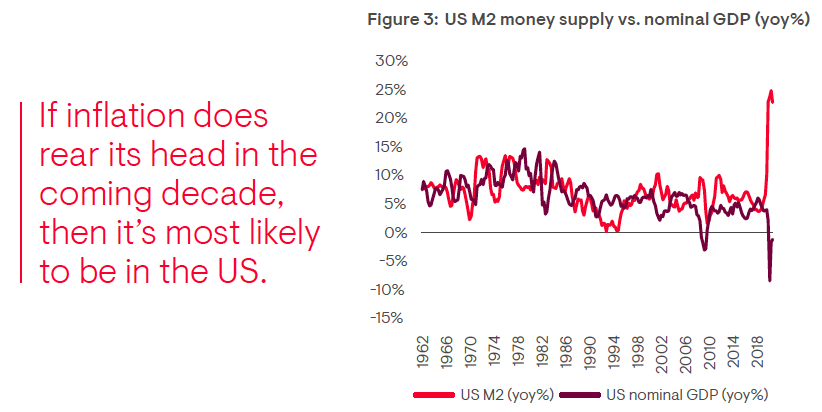

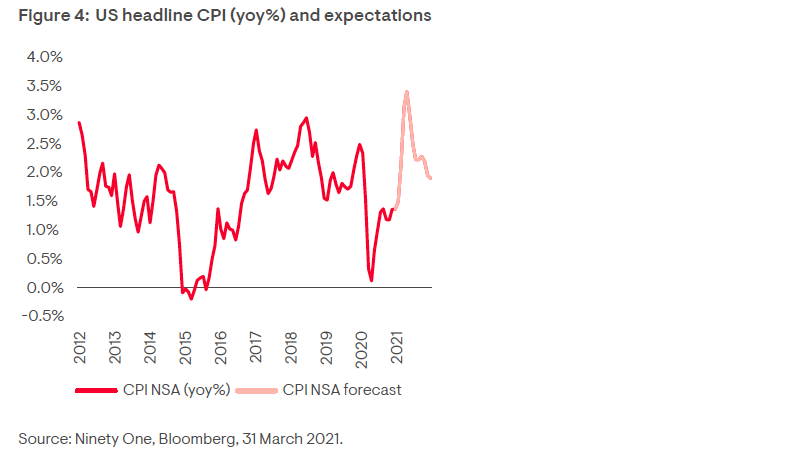

The degree of stimulus and the corresponding growth in money supply (Figure 3) raises questions about how inflation will evolve in the coming years. Over the next few months, we expect inflation to accelerate sharply (Figure 4). However, this is largely a function of mechanistic base effects in the calculation of inflation statistics; prices plummeted dramatically a year ago. We anticipate that inflation will peak in early summer of this year (northern hemisphere), before falling thereafter, and expect major central banks to view this as transitory. Over the medium term, our expectations are detailed in our paper “Assessing inflation in a post-pandemic world”, where we highlight that a durable spell of inflation takes years to form and that the inflationary decade of the 1970s had its roots in the monetary policy mistakes that began in the early 1960s.

If inflation does rear its head in the coming decade, then it’s most likely to be in the US given the structural backdrop for demographics, leverage, the health of the banking system and the degree of policy action. We believe it is far too early to tell whether the Fed and US government will act as aggressively as they are currently on a sustained basis once excess capacity in the economy is utilised though, which is what would likely be required for a sustained bout of inflationary pressure. Ultimately, we suspect not, and believe that the Fed will tighten policy once the economy is closer to full employment and post a period of core inflation being above 2%. In our view, the near-term peak in cyclical inflation will likely create investment opportunities while investors are currently looking the other way (i.e. positioning for higher inflation).

PAY CLOSE ATTENTION TO CHINA

Another area that we monitor closely is China’s economic evolution. China is further into its economic recovery, having managed COVID-19 more effectively earlier on, and policy makers are ultimately seeking to enact more orthodox policy relative to other major nations. Chinese policy was eased notably in the first half of last year before the People’s Bank of China (PBoC) took a step back last July, towards a more neutral policy stance. Chinese authorities are now in the process of moving their credit cycle into a down phase by reducing the pace of credit issuance (a primary policy lever in China). The Chinese credit cycle has strongly influenced the global cycle and risk-on/off periods in asset markets over the past decade. The leads and lags feeding into economic growth are typically 9-12 months, so the impact will take a while to be felt, but we remain cognisant that the pace of Chinese economic growth will likely be moderating into next year.

On balance, we believe the outlook for growth assets remains constructive over the next year and we continue to bias our strategies in this direction. Economic growth is likely to be strong, policy is set to remain easy and cyclical inflation should peak in the coming months, in our view. We will continue to monitor China’s credit cycle, the progress in vaccine roll-outs and the willingness of central banks to maintain highly accommodative policy as the economic recovery accelerates, believing that these are the primary forces driving financial markets from here.

All information provided is product related and is not intended to address the circumstances of any particular individual or entity. We are not acting and do not purport to act in any way as an advisor or in a fiduciary capacity. No one should act upon such information without appropriate professional advice after a thorough examination of a particular situation. This is not a recommendation to buy, sell or hold any particular security. Collective investment scheme funds are generally medium to long term investments and the manager, Ninety One Fund Managers SA (RF) (Pty) Ltd, gives no guarantee with respect to the capital or the return of the fund. Past performance is not necessarily a guide to future performance. The value of participatory interests (units) may go down as well as up. Funds are traded at ruling prices and can engage in borrowing and scrip lending. The fund may borrow up to 10% of its market value to bridge insufficient liquidity. A schedule of charges, fees and advisor fees is available on request from the manager which is registered under the Collective Investment Schemes Control Act. Additional advisor fees may be paid and if so, are subject to the relevant FAIS disclosure requirements. Performance shown is that of the fund and individual investor performance may differ as a result of initial fees, actual investment date, date of any subsequent reinvestment and any dividend withholding tax. There are different fee classes of units on the fund and the information presented is for the most expensive class. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Where the fund invests in the units of foreign collective investment schemes, these may levy additional charges which are included in the relevant Total Expense Ratio (TER). A higher TER does not necessarily imply a poor return, nor does a low TER imply a good return. The ratio does not include transaction costs. The current TER cannot be regarded as an indication of the future TERs. Additional information on the funds may be obtained, free of charge, at www.ninetyone.com. The Manager, PO Box 1655, Cape Town, 8000, Tel: 0860 500 100. The scheme trustee is FirstRand Bank Limited, RMB, 3 Merchant Place, Ground Floor, Cnr. Fredman and Gwen Streets, Sandton, 2196, tel. (011) 301 6335. A feeder fund is a fund that, apart from assets in liquid form, consists solely of units in a single fund of a collective investment scheme which levies its own charges which could then result in a higher fee structure for the feeder fund. The fund is a sub-fund in the Ninety One Global Strategy Fund, 49 Avenue J.F. Kennedy, L-1855 Luxembourg, Grand Duchy of Luxembourg, and is approved under the Collective Investment Schemes Control Act. Ninety One SA (Pty) Ltd is an authorised financial services provider and a member of the Association for Savings and Investment SA (ASISA). The full details of the award are available on request. This document is the copyright of Ninety One and its contents may not be re-used without Ninety One’s prior permission. Ninety One Investment Platform (Pty) Ltd and Ninety One SA (Pty) Ltd are authorised financial services providers. Issued, May 2021.